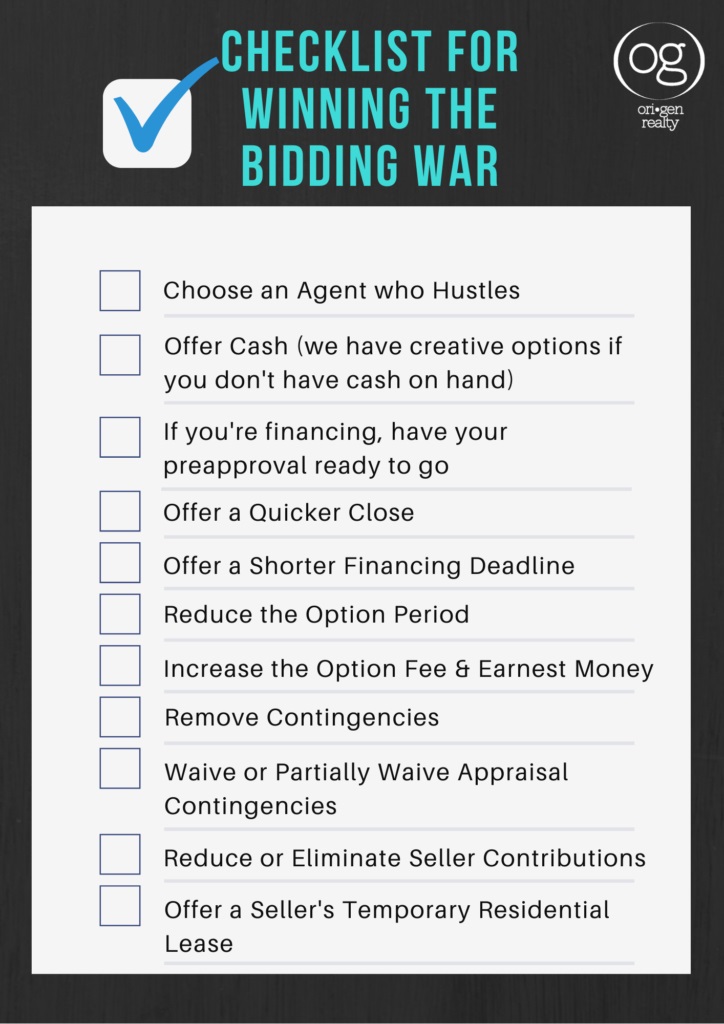

If you’ve recently made an offer to purchase a home, it’s likely that you’ve found yourself in the middle of a bidding war. That’s because record low interest rates have made homeownership affordable and created a huge demand amongst buyers. The available inventory of homes for sale, however, is at record lows. Often times, multiple buyers are vying for the same property, creating an extremely competitive atmosphere. It can be disappointing to find the home of your dreams, only to lose out to a buyer who made a more compelling offer. Obviously, offering the highest sales price seems like the most logical way to winning a bidding war, but sometimes that’s not a wise decision, or simply not possible. Here are several strategies to consider to strengthen your offer.

BE PREPARED

While always important, it’s even more imperative in this challenging market to get pre-approved with a lender before you even begin your home search. In hot markets, homes are going under contract so quickly that there sometimes isn’t a minute to spare. You’ll want to have your pre-approval ready in advance so that you can pull the trigger just as soon as you find the perfect home.

You may even ask the lender to begin underwriting your loan in advance of finding a home to expedite the home purchase and further strengthen your offer. During the underwriting process, the lender will analyze and verify your employment, income, assets, and debts, among other things. If the lender can perform some of these functions early on, you may be able to offer the seller a quicker close. Not every seller has the same motivations. If you’re able to purchase the home weeks sooner than a buyer who may have offered a slightly higher sales price, your offer may be more appealing to a seller whose primary motivation is to sell quickly.

Also, if the lender is able to begin an early underwriting of your loan, you might consider offering a shorter financing deadline in your offer. The financing deadline is the amount of time that a buyer has to obtain final loan approval to purchase the home. The financing deadline is negotiable, but 21-25 days from the date a contract is signed is a typical amount of time. If the lender determines that the buyer cannot obtain final financing approval before that deadline, the buyer will receive a refund of their earnest money. If you’re comfortable that your lender has adequately reviewed your financial situation and feel confident that you will receive final loan approval, you might consider reducing the number of days for the financing period to demonstrate to the seller your willingness to purchase.

REDUCE THE OPTION PERIOD AND INCREASE THE OPTION FEE

Most purchase contracts will include an option period, giving the buyer a designated amount of time to back out of the contract for any reason and receive a refund of their earnest money. The option period is most often used by buyers to obtain an inspection of the home, negotiate repairs, obtain estimates, and ultimately decide whether to move forward with the purchase or to back out. The length of the option period is negotiable, but typical option periods are between 7 and 10 days from the date the contract is signed and executed.

To further strengthen your offer, you might consider reducing the option period, giving you less time to back out of the contract, but demonstrating to the seller your seriousness to move forward with the purchase. If you do decide to reduce the number of days in your option period, make sure to have a home inspector of your choosing on standby so that you can ensure a timely inspection and enough time to evaluate your decision, while still protecting your earnest money. Some buyers even choose to forego an option period all together, but we always recommend that you have the home inspected by a licensed inspector. For your protection, get an inspection!

The buyer usually pays an option fee to the seller to “buy” this option period. The option fee is paid directly to the seller and is non-refundable even if the buyer decides to terminate the contract, but can be applied to the sales price at closing. The amount of the option fee is negotiable, but typical option fees are between $100 and $150. To strengthen your offer, you may consider offering a higher amount of option fee.

OFFER MORE EARNEST MONEY

Most purchase contracts include earnest money that a buyer pays within 3 days from the date a contract is signed and executed to demonstrate their good faith to purchase the home. The earnest money is held in an escrow account by the title company until closing, at which time it is applied to the purchase price of the home. If the buyer terminates the contract during the option period, or according to any other contingency included in the contract (like the financing deadline), the buyer may receive a refund of the earnest money. If the buyer defaults on the contract and misses contractual deadlines to terminate, however, the seller may retain the buyer’s earnest money.

The amount of earnest money a buyer pays, like every term of the contract, is negotiable, but is typically about 1% of the sales price. Increasing the amount of earnest money can strengthen your offer.

REMOVE CONTINGENCIES

Often times when a buyer currently owns a home that they need (or want) to sell before purchasing a new one, they’ll include a contingency in the contract called an Addendum for Sale of Other Property by Buyer. This addendum includes an agreed upon number of days for the buyer to attempt to sale their current home to move forward with the purchase. When the agreed upon date arrives, if the buyer has not secured a sale for their current home, they can terminate the contract and receive a refund of their earnest money. When the seller accepts an offer with this contingency, they are taking a risk that your home may not sell and may have wasted valuable time that their home could have been on the market or under contract with other serious buyers. If possible, removing the contingency to sell your current home can significantly improve your offer. Speak to your lender to see if you qualify to purchase without this contingency, and also consider whether you might be willing to take the risk of making an offer without it. Be sure to carefully analyze your budget of carrying two mortgage notes and other costs associated if the sale of your current happens after your purchase of the new home.

Purchase contracts involving financing also include a contingency regarding the appraised value of a home. Before making a mortgage loan, lenders will order an independent third party appraisal of the home to ensure that the home is actually as valuable as what you are paying and proportionately, what they are lending for the home. The Third Party Financing Addendum of a contract includes a contingency that gives the buyer the right to terminate if the appraisal comes in at a value less than what is required by the lender’s standards. You can however, include in your offer an Addendum Concerning Right to Terminate Due to Lender’s Appraisal, and agree to either completely waive or partially waive the right to terminate due to a low appraisal.

If you agree to completely waive the right to terminate due to a low appraisal, you would be responsible for paying the difference in the amount that the lender will lend and the sales price in cash. With a partial waiver, you can effectively set a limit on the amount you’d be willing to pay in cash in the event that the appraisal comes in lower than the sales price.

MONEY TALKS

Often times, buyers will ask the sellers for a seller contribution to be applied to their down payment, closing costs, or repairs. Receiving the seller contribution reduces the amount of cash the buyer is required to pay at closing. To strengthen your offer, consider reducing or, if at all possible, completely eliminating the seller contributions requested. If seller contributions are a must, you might consider increasing the sales price to compensate for the amount of contributions requested so that the seller’s bottom line remains the same.

Cash is king. Many sellers may look more favorably on a cash offer for a slightly lower amount than they would a higher offer that requires financing. As discussed, financing involves many contingencies that could potentially terminate the deal. Cash deals are considered a safer bet and can typically be closed much quicker than a transaction requiring lender financing. If it’s possible, consider offering cash to strengthen your offer.

If you don’t have the cash on hand, you might consider a creative alternative. Origen Realty can refer you to a company who can purchase the home quickly with a cash offer and “rent” the home to you while you’re securing your financing.

OFFER THE SELLER A TEMPORARY RESIDENTIAL LEASE

Some sellers may appreciate being offered a period of time after closing to move out of the home. If possible, you might consider leasing the home back to them for a fee or even for free, to give them time to move out after closing.

CHOOSE AN AGENT WHO HUSTLES

If you find yourself frustrated by how difficult it is to purchase a home in this current market, know that there are a variety of tactics to win the bidding war. With so many complexities, make sure you’re working with an agent who is willing to go to bat as your advocate and who is knowledgeable in these strategies. We don’t want you to bend over backwards to win the home of your dreams, but we can help you carefully evaluate which of these options are feasible for you. Contact us at 281.691.6177 or info(at)origenrealty(dotted)com to start developing your plan of action to win the bidding war!

***Note: I am a real estate professional, not a lawyer. Nothing herein should be construed as legal advice or instructions.